I’ll be upfront: I have a personal stake in this story. I’m Norwegian by heritage, and I’ve watched Norway navigate global disruption my entire life with a kind of quiet strategic confidence that most larger countries never quite manage. So, when the tariff environment exploded earlier this year, I was paying close attention to what Norway – and its Nordic neighbors – did next.

What I found was not what I expected. It wasn’t resilience. It wasn’t crisis management. It was opportunity capture.

Norway had less than 8% of its exports going to the US when this disruption hit. That’s not an accident. It’s the result of decades of deliberate diversification – across markets, relationships, and revenue streams – that left Norway with something most economies didn’t have when the ground shifted: a choice. While others scrambled to protect existing positions, Prime Minister Støre led a thirty-CEO trade mission to Brussels, simultaneously deepening US defense and energy partnerships, and accelerating new FTAs with Vietnam, India-EFTA, and Mercosur.

Norway didn’t react to the disruption. It moved through it.

Optionality isn’t luck. It’s what disciplined diversification looks like when it finally gets tested.

I presented on this topic at last month’s International Business Circle’s CEO and CFO Roundtable: Shifting Global Dynamics for Growth: Critical Insights for Global Leaders.

My lens was the full Nordic region – Norway, Sweden, Denmark, Finland, and Iceland. Twenty-seven million people. Five of the world’s most open, trade-dependent economies. No political cushion. No large domestic market to absorb the shock. They hit the wall before most US companies even saw it coming.

And the ones that are winning did something most leadership teams haven’t done yet. They stopped treating this as a trade problem and started treating it as a strategy problem.

The Reframe That Separates Winners from Waiters

Back in May, I spent time at the Select USA Investment Summit in Washington, D.C. Most of the conversations I had with CEOs and CFOs at the summit, as well as in other forums, all start in the same place: tariffs. What’s the exposure? How do we hedge it? When does it stabilize? Those are legitimate questions. But they’re the wrong first questions.

The instinct in a tariff environment is to manage costs and wait for clarity. Renegotiate supplier contracts. Delay capital decisions. Model scenarios. That’s risk management. It’s necessary. But it doesn’t build position. And in an environment where the rules are being rewritten, the gap between “we’re managing through it” and “we’ve fallen behind” closes faster than most leadership teams expect.

The Nordic companies that are outperforming made a different call early. They stopped asking “how do we protect what we have” and started asking “where does this environment create an opening no one else is moving into yet?”

NATO membership changed the calculus entirely. Nokia launched a dedicated defense AI unit. Patria’s armored vehicle platform was adopted across NATO. IQM Quantum moved aggressively into the US market. Finnish equities were up 23.5% in 2025 – while most of Europe contracted. The common thread: each of these companies reframed their technology as security and resilience infrastructure. That reframe made them tariff-immune, politically welcome, and first in line for a wave of NATO procurement spending that is only accelerating.

Novo Nordisk did something even bolder on the Denmark side. Facing 20%+ market declines and direct exposure to US trade policy, they didn’t lobby and wait. They negotiated. Lower drug prices in exchange for Medicare access and a tariff grace period. Whether you agree with the terms or not, that deal structure is now the template for every company in a regulated industry navigating a politicized trade environment. You don’t win by being right. You win by being in the room.

The through-line in both cases isn’t luck or scale. It’s the willingness to treat disruption as a strategy problem.

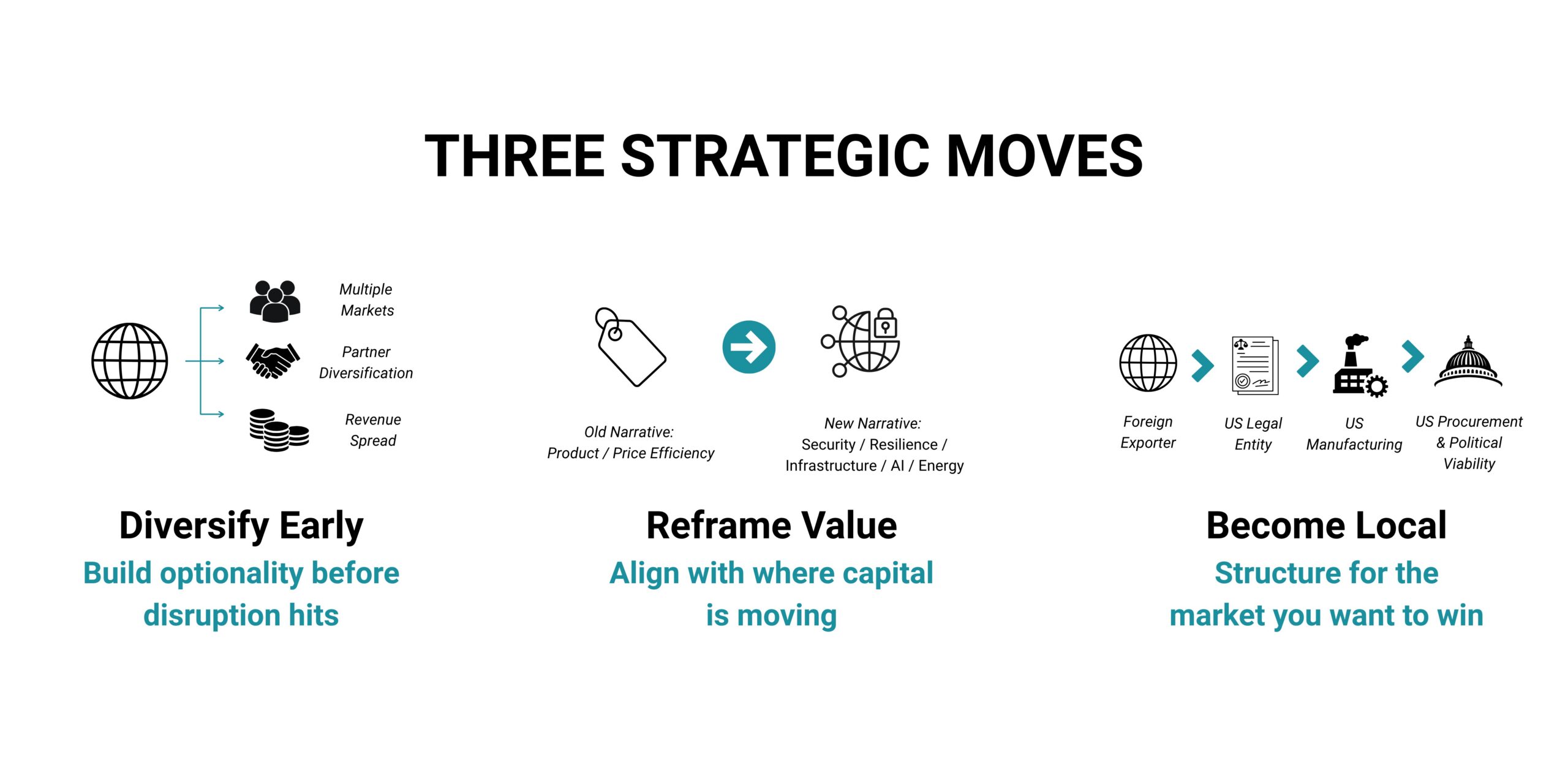

Three Strategic Moves Worth Stealing

Across the Nordic landscape, three moves keep surfacing in the companies that are pulling ahead. They’re not Nordic-specific. They’re universally applicable.

1. Diversify before you have to, not after.

Norway’s performance this year didn’t happen because of anything Norway did in 2025. It happened because of decisions made years earlier — patient, unglamorous diversification across markets, partners, and revenue streams that most leadership teams deprioritize when times are good. The payoff is strategic freedom at exactly the moment everyone else has none. The time to build optionality is before you need it. If your growth is concentrated in one market, one channel, or one customer segment, that’s not a tariff risk. It’s a strategy risk.

2. Reframe your value proposition around what the environment rewards right now.

Defense, energy security, supply chain resilience, AI infrastructure — these categories are growing regardless of tariff levels because governments and corporations are paying for them proactively. If any part of your business touches these themes, the question is whether your positioning reflects that or whether you’re still leading with the old story. The reframe isn’t a rebrand. It’s a deliberate decision to meet the market where capital and procurement attention are actually flowing — and to get there before your competitors realize the conversation has moved.

3. Stop thinking about market entry as geography. Think about it as an entity structure.

The Nordic companies succeeding in the US right now are not entering as foreign exporters. They are becoming American — US legal entities, US manufacturing where it matters, US capital relationships, and US leadership faces on the brand. Saab is building US production facilities not because it’s cheaper, but because it’s the only structure that makes you genuinely tariff-proof and politically viable at the same time. For any global company thinking about the US market, this is no longer an optional strategy. It’s table stakes.

The Question I’d Ask Your Leadership Team

The companies I’m most worried about right now are not the ones with high tariff exposure. They’re the ones with high tariff exposure and a cost-management response.

Cost management is a tactic. It buys time. It does not build position.

The Nordic experience suggests one clarifying question worth putting to your team: if this environment is permanent — not a cycle, not a negotiation, but the new baseline — what should we do differently?

The companies that thrive in the next 24 months won’t be the ones who wait for certainty. They’ll be the ones who built a strategy for a world without it.

That’s the conversation worth having. And it’s a very different conversation than tariff modeling.

Let's Talk

This is the work we do at ZELOCIN™ & Partners – helping companies cut through the noise and build a growth strategy that holds up under pressure. If this is landing for you, reach out. The first conversation is on us.

About the Author

Bjorn Leigvold is a Partner of ZELOCIN™ & Partners and the Founding Partner at Thor Global Marketing, advising global companies on market entry, go-to-market strategy, and digital transformation. He is a former Global Marketing Executive at Western Union, Wyndham Worldwide, AT&T, and UPS, an international keynote speaker at Money 2020, and an executive

coach for global leaders. He is based in Denver, Colorado.